Relying solely on a state pension will not afford you a comfortable retirement. That’s why retirement planning is essential for everyone. Consistency and time are the key ingredients to success, so the best advice is to start early, save regularly, and let time work in your favour.

Starting small is better than not starting at all

It’s a common misconception that you need a large sum to begin saving for retirement. You absolutely don’t. As with many things, getting started is the most important step, although also often the hardest.

It’s very easy to find excuses to delay saving, but this is a costly mistake. Consistency and time trump every time when it comes to retirement saving. Let’s take a look at why.

The power of compound interest

Small, regular contributions to a retirement fund grow exponentially over time. In fact, the effect is so big that time is considered to be the most valuable asset in investing.

|

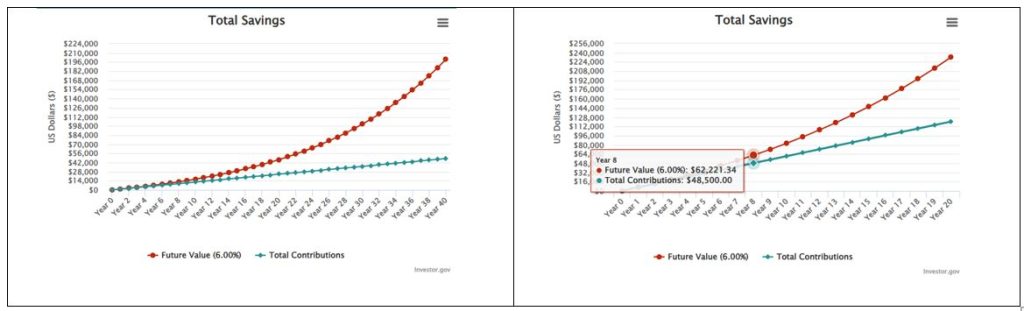

Case Study 1: Linda, early saver

|

Case Study 2: Derek, late saver |

| Linda started saving into a retirement fund aged 25. |

Derek started saving into a retirement fund aged 45.

|

|

|

| Result:

Total contributions: $48,000 Saving timeframe: 40 years Retirement pot after interest: $200,000 Growth from interest: $152,000.

|

Result:

Total contributions: $120,000 Saving timeframe: 20 years Retirement pot after interest: $233,000 Growth from interest: $113,000

|

Source https://www.investor.gov/financial-tools-calculators/calculators/compound-interest-calculator

Source https://www.investor.gov/financial-tools-calculators/calculators/compound-interest-calculator

Key takeaways:

- Despite investing significantly less, Linda’s growth from interest was $39,000 more than Derek’s.

- Linda contributed $72,000 less than Derek, but her pension pot was only $33,000 less than his.

- Derek had to invest more than double than Linda did to end up with just $33,000 more.

- Starting later significantly reduces the effect of compounding, so you need much more capital to reach the same goals.

In reality, Linda, being the sensible financial planner that she clearly is, would probably increase her monthly contributions as she progressed through her career and end up with a much larger pot.

Nevertheless, the case studies clearly demonstrate the benefits of starting to save for retirement early, even if you don’t have a huge amount to invest. Wealth is built thanks to the power of time and compounding.

Make saving a habit

Getting into a savings habit is the same as getting into any other habit, such as exercising. The psychological win of starting small with small steps makes the task feel manageable and will motivate you to carry on.

You will always find a valid excuse to delay saving:

“I’m young, I don’t need to think about saving for retirement yet.”

“I have small kids; I don’t have the headspace to think about my pension.”

“I’ll save into a pension when I’m earning more and have more disposable income.”

But the truth is that the perfect moment to start saving will never present itself. There will always be other priorities to occupy your mind or spend your money on. Whether to prioritise your future financial security is a choice that you make.

Will you get started now or continue procrastinating?

Remember, early savers have more choices – they can choose to retire earlier, reduce working hours as retirement approaches or even change career. The more savings you have, the more freedom and less stress you will have in later years.

Automation is your ally

Once you choose to prioritise savings, make life as easy as possible for yourself by automating saving each month with direct debits into a dedicated account. Set this up as soon as possible after pay day. Once the money is out of your current account, it’s less tempting to sacrifice it for purchases which might give you an immediate dopamine hit but will diminish rather than build your wealth.

Start where you are, and get help!

If you’ve been procrastinating over retirement planning because you don’t have much to invest now, the important takeaway from this article is that it’s not about how much you start saving, it’s simply that you start. A little now beats a lot later – although of course, you can always do both if you’re financially able to invest more later on!

Why not talk to an Infinity financial adviser today? They can help you work out how much you can afford to save and devise a savings and investment strategy aligned to your situation.

Don’t miss out on the benefits of compound interest – now is the time to start saving for retirement.

A leading provider of expat financial services and wealth management services across Asia.