William Gray, Infinity’s no-nonsense financial adviser in Vietnam, outlines everything you need to know about health insurance in Vietnam: why it’s essential, what to look out for when choosing a policy, and how to get help navigating the vast array of options on offer.

Health insurance: one of the foundations of a financial plan

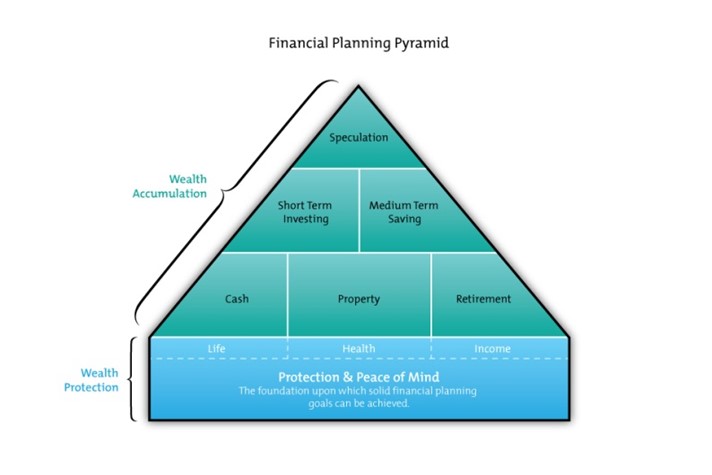

The financial planning pyramid emphasises the need to secure a solid base of wealth protection before moving on to wealth accumulation and growth strategies.

Those who fail to lay the key foundations of life insurance, health insurance and income protection, are putting themselves and their families at significant financial risk. Remove one element of the base of the pyramid, and the whole thing can quickly come tumbling down.

Imagine, for example, that you or a family member is diagnosed with a form of cancer requiring highly specialised and lengthy treatment but you don’t have health insurance. Even with a substantial amount of savings in a bank account, covering the cost of treatment out-of-pocket can rapidly deplete those funds, throwing your long-term financial plan into disarray. Especially if you have to take time off work unpaid for recovery.

I strongly advise health insurance for all my clients in Vietnam, no matter how young and healthy they are.

How does health insurance work

Health insurance protects against the risk of incurring medical expenses. If you or any member of your family covered under your medical plan become sick or incur an injury, the insurer will cover the payments for any treatment subject to any predefined exclusions.

Life is unpredictable and your medical requirements can change overnight. In addition, the cost of medical treatment is high and has consistently risen ahead of inflation for many years. Having a comprehensive health insurance policy protects your finances and offers peace of mind.

Expatriates and social security in Vietnam

While expatriates working legally in Vietnam with a work permit will have access to the Vietnamese social security system via their contributions and those of their employer, many expatriates choose not to rely on public hospitals in Vietnam which may not offer the latest effective treatment or the most up-to-date facilities.

Expatriates and group health insurance in Vietnam

Group health insurance is often provided to expatriates working in Vietnam by employers as part of their benefits package. This type of insurance offers several advantages, including comprehensive coverage, lower premiums due to pooled risk, and the convenience of employer management.

However, you should be aware that there are some disadvantages for employees. These include limited flexibility, as the plan options and coverage levels are typically predetermined by the employer, and potential gaps in coverage if your specific healthcare needs or preferences aren’t fully met by the group plan.

Additionally, coverage may end when the employment relationship terminates, requiring you to secure individual insurance to avoid gaps in protection. If you have an existing condition, this can pose a problem as it will likely be excluded from future policies.

It is possible to buy a top-up policy to bridge the gap between existing cover and extended needs.

In recent years, there has been a trend towards companies in Vietnam shunning group insurance schemes in favour of giving the cash to their employees to go it alone. If you are in this situation, I advise speaking to a professional to ensure that you are investing in a policy that meets your needs.

How private individual health insurance in Vietnam works

If you are not covered by the Vietnamese social security system or group health insurance, or you decide that the cover you have is insufficient, you will need private individual health insurance.

When you take out a medical insurance policy, the provider will ask certain questions to establish the medical histories of those to be covered and use that information to work out the monthly premium which you will have to pay.

Obviously, the older you get the more likely you are to need to claim on the policy and the higher the premiums are likely to be. Similarly, if you have a pre-existing medical condition which involves ongoing costs, your premium will reflect that or any treatment pertaining to that condition may be excluded from the policy.

That is one reason we encourage health insurance for all our clients, even the younger ones. As you age, the more likely you are to have a medical condition that will be excluded

Local versus international health insurance policies for expatriates in Vietnam

Expatriates living in Vietnam can choose between local Vietnamese health insurance plans and international health insurance plans. Each option comes with its own set of advantages and disadvantages.

Local Vietnamese health insurance plans are certainly more affordable than international plans. They will cover medical services in Vietnam, including treatment at local hospitals and clinics and are straightforward and easy to put in place.

However, coverage is limited, especially for specialised treatments or surgeries, high-cost procedures or chronic conditions. Communication with healthcare providers might be challenging if the insurance company and medical staff do not have English-speaking representatives. In addition, some local policies have numerous exclusions and restrictions, which can be problematic in the event of a serious health issue.

Although more expensive, most expatriates opt for an international health insurance plan to benefit from comprehensive coverage which includes emergency evacuations, specialist treatments, and chronic condition management.

Portability is, of course, a massive factor to consider for expatriates. International plans are valid globally, allowing expatriates to receive medical care when travelling or relocating outside Vietnam without needing additional coverage. Again, this is important if you have pre-existing conditions.

In general, international plans also provide access to private hospitals and clinics with English-speaking staff and higher standards of care.

Signing up for an international plan can be more complex, involving more paperwork and potentially longer waiting periods for certain coverages to take effect and working with a broker is advisable to navigate these complexities and ensure you have the coverage you need.

Health insurance in Vietnam: a checklist of questions

These are the points to consider when you are choosing a health insurance policy in Vietnam:

- Geographical coverage – are you covered in all the locations where you and your family will live, work, and travel?

- Do you want to include or exclude USA cover?

- Is the policy local or international?

- Pre-existing and chronic conditions – does the plan you are considering offer cover, restricted cover or full cover for a stated period. Be clear about what you are and are not covered for.

- Is there a moratorium option if you have a recent pre-existing condition that is no longer an issue?

- Is the policy individually or community-related? This relates to how premiums are calculated. Is the insurer looking at you as an individual or as part of a community? If it is a community how does your claims/health history rate against the community to which you belong?

- If you or a member of your family have got a pre-existing condition look for a Medical History Disregarded (MHD) policy. These are usually available as part of a corporate or group plan.

- Choice of hospital and treatment location – do you have a free choice of where you can seek treatment? Are repatriation and treatment in alternative countries covered?

- Do you need or want cover for outpatient care? (for example a GP or specialist care)

- Are you covered for emergency evacuation for yourself and a companion?

- How much are the annual deductibles or excess? (That is the amount of any claim you will have to cover out of your own pocket and electing to pay nil is an option).

- What is the maximum payout stated in the policy and does this differ depending on the type of claim?

- Does your insurer offer direct settlement to the healthcare provider, or do you have to pay first and claim back costs?

- If you are transferring from a group scheme to a personal policy does the policy offer continuous transfer terms with exactly the same benefits and premium?

- Is there flexibility with regard to premium payments – can you pay monthly or annually, and which would suit you best?

- In what currency can you pay the premiums?

- Are you covered for alternative or complementary medicines?

- What are the terms with regard to age limits and renewability?

- What provision is there for emergency medical advice and treatments? Many insurance providers provide hotlines and other support services.

- Are there any additional benefits such as free health checks? Ask your provider for information on availability and frequency.

- If your employer offers a medical plan, does it provide adequate cover for you and your family?

- If maternity cover is important be aware of waiting periods as they can vary for new plan holders (usually 10-12 months).

Help with health insurance in Vietnam

Nothing is more important than your health which is why it’s a good idea to speak to a professional to ensure that you have cover appropriate for your needs.

If you live in Vietnam and would like help choosing the right health insurance policy for you and your family, I’d be happy to help.

Feel free to get in touch at william.gray@infinitysolutions.com for a free, no-obligation consultation to talk through your questions. Together we can evaluate your healthcare needs, budget, and lifestyle so you can make an informed decision to safeguard your health and financial well-being while living in Vietnam and further down the line.

Financial Advisor

A British financial adviser in Vietnam, specialising in wealth and investment management for expats, with certifications in financial planning and investment, he helps clients organise their finances to enhance their lifestyle and achieve their goals.