A UK-university education is highly regarded and many local and international families in Asia desire this for their children. But it’s not cheap and needs careful planning! We’ve put together this brief guide for parents preparing to send their children to university in the UK.

The UK: a study destination of choice around the world

A recent report from UCAS (Universities and Colleges Admissions Service) in the UK reveals that international students still view the UK as a study destination of choice. Here at Infinity, we know the UK’s strong academic reputation attracts expatriate and local families in Asia alike because it is a key element of financial planning for many of our clients.

But a university education in the UK does not come cheap and working out just how much it will cost is not an easy task.

This brief guide is a useful starting point for parents preparing to send their children to university in the UK. You might want to check it out even if your children are still in nappies – the longer you have to prepare for this major financial undertaking, the better.

How to prepare for university in the UK

- Start saving early

With minimum tuition fees of £9,250 for most students in the UK (some exceptions apply) and annual rent topping £6,000 in even the least expensive towns (over £10,000 in London), a university education is costly, and rising year on year. Even for those eligible for fee and maintenance loans – and many international students won’t be – this is increasingly putting a financial strain on parents and graduates alike.

That’s why we recommend that parents hoping to fund a university education for their children, should start saving early. If possible, from birth. It’s never too early to start.

Spreading the cost over 18 years is much easier than trying to come up with tens of thousands when your child is on the cusp of adulthood and about to fly the nest. Saving earlier not only gives you longer to save but you’ll also benefit from compound interest to boost your savings.

To give an example, if you save just £100 per month over an 18-year period, total savings come to £21,600. With a 5% return, which should be achievable with the right investment advice, this can be boosted to $34,000 – enough to cover a significant chunk of the cost, depending on fee status (see below).

If you’re looking to explore setting up an education fee fund to build capital for your child’s university education, benefit from our expertise to maximise your return. We’d love to hear from you.

- Understand fee status

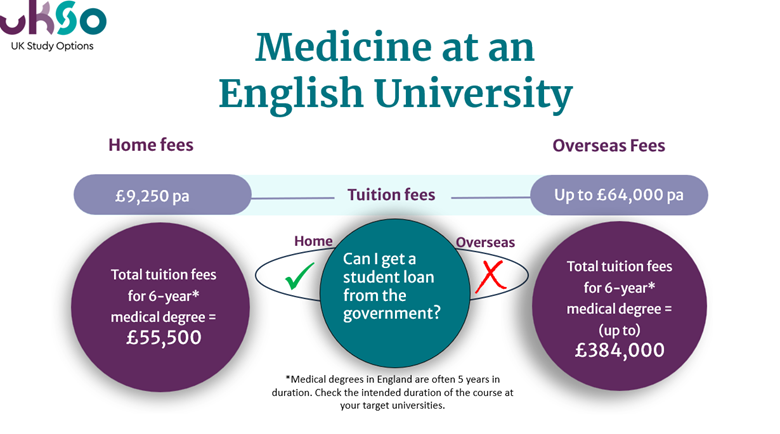

Undergraduates in the UK are deemed to be either Home or Overseas students and the fees payable are very different. In contrast to the figures outlined above, overseas students will pay between £36,000 and £384,000 in fees (2024 rates) and will have no access to student finance.

Here’s a comparison of Home and Overseas fees from UK Study Options (UKSO), one of Infinity’s trusted partners:

Myths abound regarding fee status for UK nationals. These are some of the most common ones according to Sam Goodwin, Head of Global Engagement at UKSO:

- MYTH: We’ll have to live in the UK for 3 years to get home fees

- MYTH: A British passport guarantees you home fees

- MYTH: People we know got home fees so we will too

- MYTH: We don’t have to worry about fee status until the UCAS application

- MYTH: Sending my child to boarding school in the UK will guarantee home fees

Gaining clarity on fee status is far from easy. Not only are there different rules in each UK nation but universities use their autonomy to decide fee status. While one may deem your child to be a Home student, another may decide they are subject to Overseas fees.

UKCISA (the UK Council for International Affairs) is a goldmine of information for international students. They warn that students may have to persuade institutions that they meet the Home fees requirements.

You’ll find links to the full rules and regulations for fee status on the UKCISA website but in most, cases, to qualify for Home status in the UK, an expatriate student must be able to show an ‘ordinary residence’, usually in the UK, for the three year period before the start of the university course. In some cases, they may be able to demonstrate that their absence from this ordinary residence is only temporary which could allow home fees to be given.

Sam Goodwin has written a useful article about what ordinary residence means for expatriate families.

Parents serious about their child studying in the UK should plan ahead and implement a fee status strategy comprising the following steps:

- Consider eligibility as early as possible

- Build your case and gather evidence

- Be prepared to appeal Overseas offers

- Get personalised, specialist advice

Working with a specialist such as UKSO can increase the likelihood of your child qualifying for Home fees and save thousands in tuition fees as well as speeding up offers from university.

Thursday June 20th 2024 – Join our Webinar for parents preparing to send their children to university in the UK

In this article, we’ve given just a brief overview of the issues facing parents preparing to send their children to university in the UK. Having hosted three highly successful events across Asia on this subject, we know that this is a hot topic for our clients. That’s why we are preparing an informative webinar to provide further information for those of you who were unable to attend in person. If you’d like to attend, you can register here.

And if you have any questions about education fee planning, don’t hesitate to get in touch.

A leading provider of expat financial services and wealth management services across Asia.