The importance of early retirement planning cannot be over emphasised. Time is the ingredient that enables compound interest to work its magic on your pension savings. And the difference in return if you start early can be astonishing, as Robin Copley explains.

Expat life in Vietnam: a golden opportunity to save

I recently came across an interesting statistic in the HSBC Expat Explorer Survey: only 25% of expats begin retirement planning within the first five years of moving abroad.

That means that 75% of expats are missing out on a golden opportunity to save and invest for retirement.

Here in Vietnam, expat life is sweet, often combining a sizeable income with a low cost of living (we recently topped the charts on the personal finance index of Internations’ annual Expat Insider Survey), leaving expats with more disposable income than they would enjoy back home.

And there is no shortage of ways to spend it. From weekend getaways in jaw-dropping destinations around Asia, to indulging in fancy high-end restaurants and sipping cocktails in the hottest new bars, it’s easy for your spending to creep up and match your income.

Of course, as an expat, you should absolutely soak up every bit of this adventure. After all, that’s part of the experience! But while it’s tempting to say yes to every trip and spontaneous splurge, striking a balance is key.

Spare a thought for your future self and allocate some of that disposable income to saving for retirement.

Be a Jane, not a John!

John’s story: how not to save for retirement!

John moved to Vietnam at the age of 25. He worked hard and played harder – he was having too good a time to think about saving for retirement. He figured there would be plenty of time for all that later on. Instead, he spent every cent he earnt on indulging himself.

Then middle age hit, and he panicked. At 40 years of age, not only did he have a family to support, school fees to pay and a mortgage but he also started to realise that, suddenly, retirement didn’t seem so far off, and he had no pension to speak of.

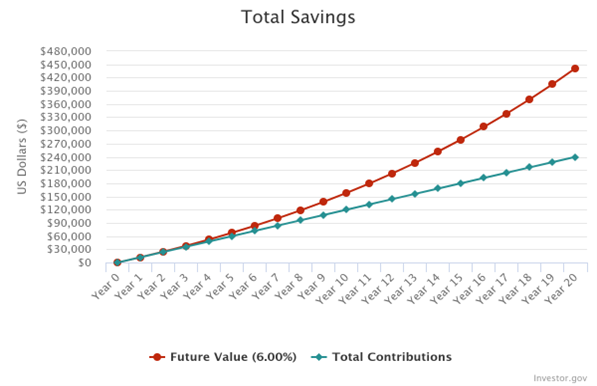

So, John started saving $1000 a month. He invested it over 20 years, earning a return after inflation of 6%. He retired at 60 with a pension pot of $441,427.09 in today’s money.

Jane’s story: how to save for retirement!

Jane also moved to Vietnam at the age of 25. She worked hard and had a great time too, but she was a planner and decided to save $1000 a month from the get-go.

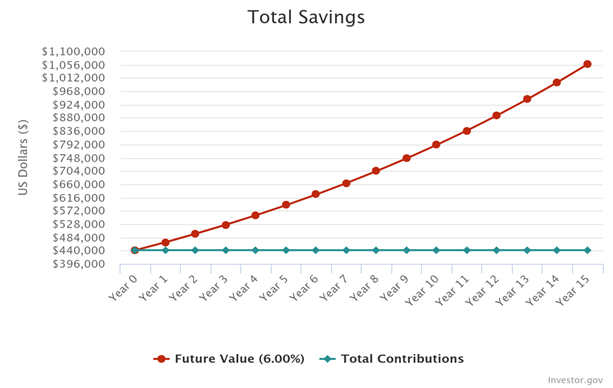

By 45, she had amassed a pension pot of $441,427.09 – the same amount as John over the same 20 year time period.

But this is where it gets interesting!

Just so we can compare like with like, let’s say Jane stopped saving at 45 (I don’t generally recommend this!). Her pension pot sat untouched for another 15 years, during which time her savings grew and grew, earning an average return of 5%. By the time she retired, also at 60, she had amassed $1,057,905.71.

Both John and Jane invested a total amount of $240,000 over 20 years.

But while John made a return on investment of $201,427.09, Jane’s return was over four times more at $817,905.71.

The only difference: the investment timeframe. Jane’s savings were made 15 years earlier, giving her 35 years of compound growth compared to John’s 20.

Compounding: your retirement saving friend

Compounding: your retirement saving friend

Now we all know that life isn’t this simple – few 25 year olds save $1000 every month! Generally as we age, we save more in line with our earnings increases, but the point here is Jane’s savings grew so much more due to compound interest.

Given time, compounding can bring about astonishing increases in the worth of an investment. And the more time it has to work, the bigger the effect. That’s why expats who start planning for retirement before the age of 40 are twice as likely to achieve their retirement goals.

If you put off saving until you are in your 40s or later, you miss out on decades of compounded returns, which could mean having to make lifestyle compromises in retirement.

My advice is simple: whatever your age, now is the best time to start saving for retirement.

If you’re a high earner with children, it’s also worth considering setting aside savings for them early on. Even modest contributions can grow significantly over time, giving them a massive head start in building their own future wealth 20 years from now.

Retirement savings advice in Vietnam

If you’re unsure where to put your retirement savings, that’s where I come in. I will help you safeguard your wealth and ensure that you can retire with dignity, safe in the knowledge that you will never run out of money.

With a wealth of knowledge on cross-border finances and the challenges faced by expats in Vietnam, I am perfectly placed to give you advice tailored to your unique situation.

If you’re ready to start saving and investing to avoid a big financial planning mistake that you’ll pay for later, get in touch for a chat.

Financial Consultant

Level 4 Investment Advice Diploma from the Chartered Institute for Securities & Investment,

with a specialism in Financial Planning